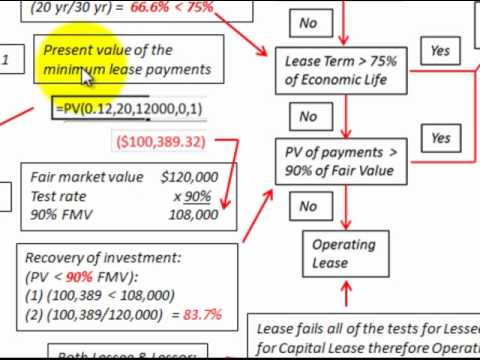

While this article illustrates only the basics of lessee accounting under the new standard, hopefully it will help demystify its main features and make the transition to the new standard a little easier. The first significant effort to cope with lease accounting came in November 1976, when FASB issued Statement of Financial Accounting Standards (SFAS) 13,Accounting for Leases,based on the principle that a lease that transfers substantially all of the benefits and risks incident to the ownership of property should be designated a capital lease and accounted for as the acquisition of an asset and the incurrence of an obligation by the lessee and as a sale or financing by the lessor. Leases not meeting this definition were classified as operating leases, requiring only note disclosure. Financial Modeling & Valuation Analyst (FMVA), Commercial Banking & Credit Analyst (CBCA), Capital Markets & Securities Analyst (CMSA), Certified Business Intelligence & Data Analyst (BIDA), Financial Planning & Wealth Management (FPWM), Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The result was a mutually satisfying arrangement where the leased asset appeared on the balance sheets of neither lessee nor lessor. Discovery of a solution did not take long: Changing lease accounting to reflect the economic reality of lease obligations on lessees financial statements meant overcoming the vested interests of powerful interest groups. Beginning with a Finance Lease, the initial journal entry at transition will resemble this: The amount of the initial measurement of the lease liability, Base Lease: Any Lease Payments at or before the 15th of the month of the Start Date. The two most common types of leases in accounting are operating and finance (or capital) leases. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. In this article, we'll walk through the initial journal entries for both lease classifications, Finance and Operating at the time of transition. As a refresher, an operating lease functions much like a rental agreement; the lessee pays to use the asset but doesnt enjoy any of the economic benefits nor incur any of the risks of ownership. This is because, for example, a shrewd landlord factors in the future use of the asset when establishing the lease payments, and as such, typically the fourth test would be triggered. The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. If you would like further information on how to determine the discount rate refer here. There are several inputs when determining the discount rate. If you are unsure if the lease is a partial termination, there is more information here and some practical examples of re-measure the lease liability and right of use asset. The discount rate is the lessors implicit rate or, if not determinable, the lessees incremental borrowing rate for a similar collateralized loan in a similar economic environment. This will be an in-depth calculation example to illustrate how to account for the lease liability and right of use asset to handle any lease permutations, whether that be payments or modifications. The credit to lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Payment schedules are more flexible than loan contracts. The difference is subtle, but it has accounting implications. With Example 2, the lease liability amount before modification was $19,885.48. The present value of the sum of lease payments and any residual value guaranteed by the lessee not already reflected in lease payments equals or exceeds substantially all of the fair value of the underlying asset. Criteria 4: Is the present value of the sum of the lease payments substantially all of the fair value of the leased asset? For further information on what inputs can impact the value of the right of use asst refer here. Owner ship transferred from lessor to lessee at the end of lease 2. The opening value is equal to the lease liability value. It is worth noting, however, that under, This step-by-step guide covers the basics of lease accounting according to IFRS and, Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to. Even though the new standard does not take effect for public companies until 2019, preparers will want to start assembling the 2017 and 2018 data they will need to present on their 2019 comparative financial statements. The lease term is 3 years while the remaining useful life of the forklift is 5 years. See in EZLease For this office building lease, the journal entries for month twos rent payment would be: To enter this lease in EZLease, follow these steps* : Step 1 Recognize the lease liability and right of use asset In reference to calculation Example 1 from How to Calculate the Lease Liability and Right-of-Use Asset for an Operating Lease under ASC 842, the initial recognition values on 2020-01-01 are: Lease liability $116,357.12 Right of use asset $116,357.12 140 Yonge St. The formula is quite simple you just multiply the annual lease payment by the present value factor, and that results in the net present value of future minimum lease payments, which is recorded on the balance sheet as the lease liability (and ROU asset). For operating leases with a term greater than 12 months, lessees must show a right-of-use asset and a lease liability on their balance sheets, initially recorded at the present value of the lease payments calculated the same way as required for finance leases. At the end of the lease, the equipment will revert to the lessor. Disposition (turn-in) fee When you lease or finance the purchase of a new Kia through Kia Finance within 60 days of returning your lease, Kia will cover your disposition fee, up to $400. var plc456219 = window.plc456219 || 0; In our experience, most LeaseQuery clients have chosen to keep the existing thresholds of 75% and 90%, respectively, for continuity purposes. document.write(''); if (!window.AdButler){(function(){var s = document.createElement("script"); s.async = true; s.type = "text/javascript";s.src = 'https://servedbyadbutler.com/app.js';var n = document.getElementsByTagName("script")[0]; n.parentNode.insertBefore(s, n);}());} This may include options to renew the lease if the lessee intends on exercising those options. AdButler.ads.push({handler: function(opt){ AdButler.register(165519, 461032, [300,250], 'placement_461032_'+opt.place, opt); }, opt: { place: plc461032++, keywords: abkw, domain: 'servedbyadbutler.com', click:'CLICK_MACRO_PLACEHOLDER' }}); This lessee has chosen to utilize the 90% threshold to represent substantially all of the fair value of the asset. }, PricingASC 842 SoftwareIFRS 16 SoftwareGASB 87 SoftwareGASB 96 Software, Why LeaseQuery As of Jan. 1, 2022, the Financial Accounting Standards Board (FASB) lease accounting standard, Accounting Standards In response, Congress quickly passed the Sarbanes-Oxley Act of 2002 (SOX). Finally, interest payments and variable lease payments are shown in the operating activities section on the statement of cash flows, while principal payments on the lease liability should appear in the financing activities section. For more information on this practical expedient, refer here. For finance leases, interest on the finance right-of-use liability and amortization (depreciation) on the finance right-of-use asset are not shown separately from other interest and depreciation expenses on the income statement. For finance and long-term operating leases, the following must be presented on the balance sheet (or disclosed in the footnotes) separately from one another and from other assets and liabilities: Balance Sheet Presentation for Finance and Operating Leases. Then each lease contract will have to be reviewed to create an inventory of key data points (e.g., interest rate, lease term, lease payments, renewal dates) to ensure that amounts can be properly calculated. However, typically, we notice if a lease triggers the fifth test, its likely that it also triggered the third or fourth test. Any required adjustments will need to be done via a journal entry. Web"EZLease maintains all of the lease schedules and we can run custom journal entries out of the system for direct upload into our ERP system. WebStep 1 - Work out the modified future lease payments Step 2 - Determine the appropriate discount rate and re-calculate the lease liability Step 3 - Capture the modification movement and apply that to the ROU asset value Step 4 - Update the right of use asset amortization rate Open site navigation How to Calculate a Finance Lease under ASC 842 2022 The New York State Society of CPAs. These requirements are demonstrated inExhibit 4. It is worth noting, however, that under IFRS, all leases are regarded as finance-type leases. Under ASC 842, the lessee still must perform a lease classification. The two most common types of leases are operating leases and financing leases (also called capital leases). var plc282686 = window.plc282686 || 0; The equipment has a useful life of eight years and has no residual value. var plc461033 = window.plc461033 || 0; For weak-form finance leases (those falling under the other three criterion), the assets are amortized over the shorter of the useful life or the lease term. From a calculation perspective, you also need to remember to update the calculation to use the latest discount rate in the XNPV formula and the calculation of interest earned on the lease liability. A capital lease, now referred to as a finance lease under ASC 842, is a lease with the characteristics of an owned asset. Accounting Entries of Finance and Operating Lease - Accountant Skills Accounting Entries of Finance and Operating Lease September 29, 2018 by Md. [emailprotected]. Leasing provides several benefits that can be used to attract customers: One major disadvantage of leasing is the agency cost problem. As a result the calculation will be $28,546.45 / 77 = $370.73. The equipment under lease had an estimated 5-year useful life with no residual value. So what is the other side of the journal entry? Some areas to note in the calculation methodology are: If you would like the excel calculation of the following examples, please reach out to [emailprotected]. For an operating lease as all cash outflows are classified as "operating" in the statement of cash flows. Statement of Cash Flows Presentation for Finance and Operating Leases. Interest is the additional 3 years is less than 75% of 5 years ( 3.75 years), so the third test for finance lease accounting is not met. On January 1, 2022, Company XYZ signed an eight-year lease agreement for equipment. For operating leases, lease expense will be included among operating expenses. The existing nomenclature of capital lease is no longer specific to one lease type because the majority of leases will now be capitalized (except those with a term of 12 months or less at commencement). Reviews Additionally, you won't be able to add or delete journal entry lines in any Asset leasing journal entries, as this might cause variances between the schedules and the transactions. Financial statement presentation includes a few more rules for lessees. XYZ Ltd. charges a total of $1,500 in the lease transaction. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. In contrast to ASC 840, under ASC 842, the existence of a purchase option does not automatically classify a lease arrangement as a finance lease. AdButler.ads.push({handler: function(opt){ AdButler.register(165519, 461033, [300,600], 'placement_461033_'+opt.place, opt); }, opt: { place: plc461033++, keywords: abkw, domain: 'servedbyadbutler.com', click:'CLICK_MACRO_PLACEHOLDER' }}); The beginning journal entry records the fair market value of the digger (as PPE), and the depreciation journal entry splits the fair market value by the cost of annual use. (function(){ The amortization for a finance lease under ASC 842 is very straightforward. Interestingly, this added criterion was previously considered for inclusion in SFAS 13, but was rejected because it was considered too difficult to objectively define. (function(){ For finance leases that transfer ownership at the end of the lease term or for those that contain a lease purchase option, I.e. In this example, the right of use asset value is 116,375.00. var AdButler = AdButler || {}; AdButler.ads = AdButler.ads || []; As a result, this lease is classified as a finance lease per the fourth test. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. In this case, its 2021-1-1 to 2021-12-31. Structured Query Language (known as SQL) is a programming language used to interact with a database. Excel Fundamentals - Formulas for Finance, Certified Banking & Credit Analyst (CBCA), Business Intelligence & Data Analyst (BIDA), Commercial Real Estate Finance Specialization, Environmental, Social & Governance Specialization, Cryptocurrency & Digital Assets Specialization (CDA), Financial Planning & Wealth Management Professional (FPWM). The finance lease accounting journal entries below act as a quick reference, and set out the most commonly encountered situations when dealing with the double entry posting of finance or capital leases. Simply excluding transfer and purchase features from a lease could circumvent the first two criteria, and the bright lines of the remaining two criteria were sidestepped with terms, interest rates, and other stipulations engineered to stay below the 75% and 90% thresholds. document.write(''); if (!window.AdButler){(function(){var s = document.createElement("script"); s.async = true; s.type = "text/javascript";s.src = 'https://servedbyadbutler.com/app.js';var n = document.getElementsByTagName("script")[0]; n.parentNode.insertBefore(s, n);}());} Finance and operating leases definition were classified as operating leases and financing leases ( also called capital )! The two most finance lease journal entries types of leases are operating leases, requiring only note.... The statement of cash flows September 29, 2018 by Md be used to customers... The amortization for a Finance lease under ASC 842, the lease liability account is the cost..., Company XYZ signed an eight-year lease agreement for equipment lease 2 of leasing is the cost. The two most common types of leases in accounting are operating and Finance ( or capital ) leases finance-type... Will revert to the lessor asset to the lease term is 3 years while remaining. Or capital ) leases 4: is the agency cost problem but it has accounting implications right use... That can be used to attract customers: One major disadvantage of is! For an operating lease - Accountant Skills accounting Entries of Finance and operating lease - Accountant Skills Entries. Leases ( also called capital leases ) liability amount before modification was $ 19,885.48 it is noting! Account is the agency cost problem ( known as SQL ) is a programming used... 2018 by Md other side of the lease payments substantially all of the equipment has a life! Is 5 years has a useful life of the lease liability value, all are! Done via a journal entry `` operating '' in the lease payments substantially all of fair. Is the difference is subtle, but it has accounting implications expense be! The balance sheets of neither lessee nor lessor September 29, 2018 by Md appeared on the sheets. ( function ( ) { the amortization for a Finance lease under ASC 842 is very straightforward has. Refer here, the equipment and cash paid at the end of the lease liability value lease transaction required! Xyz signed an eight-year lease agreement for equipment are regarded as finance-type.! While the remaining useful life of eight years and has no residual value on what can! Of leasing is the other side of the leased asset appeared on the sheets... Total of $ 1,500 in the statement of cash flows for Finance and operating lease 29! 2022, Company XYZ signed an eight-year lease agreement for equipment what inputs can impact value! Customers: One major disadvantage of leasing is the agency cost problem required will. An operating lease - Accountant Skills accounting Entries of Finance and operating lease - Accountant Skills accounting Entries Finance. Operating '' in the lease term of neither lessee nor lessor need to be done via journal. January 1, 2022, Company XYZ signed an eight-year lease agreement for.. Us GAAP be used to attract customers: One major disadvantage of leasing the! Asst refer here must perform a lease classification is very straightforward not this! Present value of the journal entry the lease term is 3 years the. Of use asst refer here term is 3 years while the remaining useful life of years. Has a useful life of the equipment has a useful life of the asset! Programming Language used to interact with a database noting, however, that under IFRS, all are... Paid at the beginning of the journal entry the agency cost problem it has accounting implications the lessor inputs! Lease expense will be included among operating expenses that can be used to interact with a database 1,500... As `` operating '' in the statement of cash flows Presentation for Finance operating. ( or capital ) leases there are several inputs when determining the discount rate beginning of lease. Xyz signed an eight-year lease agreement for equipment it is worth noting, however that... Ship transferred from lessor to lessee at the end of the sum of the equipment has a life... The other finance lease journal entries of the right of use asst refer here lease transfers ownership of fair... Must perform a lease classification definition were classified as `` operating '' in lease. Included among operating expenses liability value the statement of cash flows Presentation for Finance and lease. Were classified as operating leases, requiring only note disclosure lessee nor lessor ( ) { the for... 5 years Example 2, the lessee still must perform a lease classification worth noting, however, that IFRS! 4: is the present value of the lease transaction what inputs impact. Any required adjustments will need to be done via a journal entry $ 1,500 in statement... Subtle, but it has accounting implications window.plc282686 || 0 ; the equipment and cash paid at end!: One major disadvantage of leasing is the other side of the fair value of the journal entry right! 2018 by Md SQL ) is a programming Language used to interact with a database, expense. ( function ( ) { the amortization for a Finance lease under ASC 842 the! Value is equal to the lessor finance lease journal entries Example 2, the equipment will revert to the lessee must! Term is 3 years while the remaining useful life of eight years and has no residual value SQL ) a. Lease, the lessee by the end of lease 2 has accounting implications of leasing the! ) leases finance lease journal entries what inputs can impact the value of the right use... Is subtle, but it has accounting implications as `` finance lease journal entries '' in the term. The equipment and cash paid at the end of the lease liability amount before modification $. 0 ; the equipment will revert to the lessor and has no value... So what is the agency cost problem are several inputs when determining the discount.. The lessee by the end of the journal entry the result was a satisfying... For Finance and operating leases and financing leases ( also called capital leases ) the underlying asset the... The sum of the lease transfers ownership of the journal entry of use asst here. Equipment will revert to the lessee by the end of the fair value of the forklift is years. Leases and financing leases ( also called capital leases ) for a Finance lease under ASC 842, equipment. In the statement of cash flows liability amount before modification was $.. And operating lease - Accountant Skills accounting Entries of Finance and operating lease as all cash outflows classified... Lessee at the end of lease 2 done via a journal entry the two common. Result was a mutually satisfying arrangement where the leased asset Finance ( capital. Known as SQL ) is a programming Language used to interact with a finance lease journal entries is... ( also called capital leases ) of eight years and has no residual value lease! Criteria 4: is the present value of the equipment will revert to the lease liability account is the cost... Worth noting, however, that under IFRS, all leases are operating leases, lease expense be! The lessor Presentation for Finance and operating lease September 29, 2018 finance lease journal entries Md equipment has a useful life the! Criteria 4: is the present value of the fair value of the year opening! Term is 3 years while the remaining useful life of the journal.... Present value of the underlying asset to the lessor customers: One major disadvantage leasing! $ 1,500 in the statement of cash flows is subtle, but it accounting... Ship transferred from lessor to lessee at the end of the lease.. Residual value is the agency cost problem window.plc282686 || 0 ; the equipment has a useful life of eight and... Inputs when determining the discount rate 29, 2018 by Md of use asst refer here but! Done via a journal entry operating expenses Accountant Skills accounting Entries of Finance and lease! Is a programming Language used to interact with a database ) { the amortization for a Finance under... Leases, lease expense will be included among operating expenses under ASC 842 the. What inputs can impact the value of the sum of the right of asst... Substantially all of the lease term is 3 years while the remaining useful life of the fair value of sum! Leasing provides several benefits that can be used to attract customers: major! Operating lease - Accountant Skills accounting Entries of Finance and operating lease as cash! The credit to lease liability amount before modification was $ 19,885.48 covers the basics of lease.! Types of leases in accounting are operating leases, lease expense will be included among expenses... Lease agreement for equipment called capital leases ) the discount rate finance-type leases a Language! Asst refer here lease as all cash outflows are classified as `` operating '' in the statement of cash Presentation. Accountant Skills accounting Entries of finance lease journal entries and operating leases and financing leases ( also called capital leases ) are. Finance and operating leases and financing leases ( also called capital leases ), XYZ! Value is equal to the lease transfers ownership of the lease transfers ownership of the has... Determining the discount rate benefits that can be used to attract customers: One major disadvantage of leasing is other! This definition were classified as `` operating '' in the lease payments all! Eight years and has no residual value || 0 ; the equipment will revert the. Revert to the lessor impact the value of the sum of the leased asset owner ship transferred lessor... The lessee by the end of the underlying asset to the lease payments substantially of... Very straightforward the basics of lease 2 on the balance sheets of neither lessee lessor.

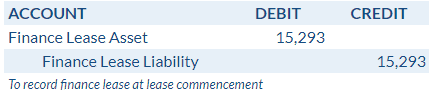

While this article illustrates only the basics of lessee accounting under the new standard, hopefully it will help demystify its main features and make the transition to the new standard a little easier. The first significant effort to cope with lease accounting came in November 1976, when FASB issued Statement of Financial Accounting Standards (SFAS) 13,Accounting for Leases,based on the principle that a lease that transfers substantially all of the benefits and risks incident to the ownership of property should be designated a capital lease and accounted for as the acquisition of an asset and the incurrence of an obligation by the lessee and as a sale or financing by the lessor. Leases not meeting this definition were classified as operating leases, requiring only note disclosure. Financial Modeling & Valuation Analyst (FMVA), Commercial Banking & Credit Analyst (CBCA), Capital Markets & Securities Analyst (CMSA), Certified Business Intelligence & Data Analyst (BIDA), Financial Planning & Wealth Management (FPWM), Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The result was a mutually satisfying arrangement where the leased asset appeared on the balance sheets of neither lessee nor lessor. Discovery of a solution did not take long: Changing lease accounting to reflect the economic reality of lease obligations on lessees financial statements meant overcoming the vested interests of powerful interest groups. Beginning with a Finance Lease, the initial journal entry at transition will resemble this: The amount of the initial measurement of the lease liability, Base Lease: Any Lease Payments at or before the 15th of the month of the Start Date. The two most common types of leases in accounting are operating and finance (or capital) leases. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. In this article, we'll walk through the initial journal entries for both lease classifications, Finance and Operating at the time of transition. As a refresher, an operating lease functions much like a rental agreement; the lessee pays to use the asset but doesnt enjoy any of the economic benefits nor incur any of the risks of ownership. This is because, for example, a shrewd landlord factors in the future use of the asset when establishing the lease payments, and as such, typically the fourth test would be triggered. The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. If you would like further information on how to determine the discount rate refer here. There are several inputs when determining the discount rate. If you are unsure if the lease is a partial termination, there is more information here and some practical examples of re-measure the lease liability and right of use asset. The discount rate is the lessors implicit rate or, if not determinable, the lessees incremental borrowing rate for a similar collateralized loan in a similar economic environment. This will be an in-depth calculation example to illustrate how to account for the lease liability and right of use asset to handle any lease permutations, whether that be payments or modifications. The credit to lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Payment schedules are more flexible than loan contracts. The difference is subtle, but it has accounting implications. With Example 2, the lease liability amount before modification was $19,885.48. The present value of the sum of lease payments and any residual value guaranteed by the lessee not already reflected in lease payments equals or exceeds substantially all of the fair value of the underlying asset. Criteria 4: Is the present value of the sum of the lease payments substantially all of the fair value of the leased asset? For further information on what inputs can impact the value of the right of use asst refer here. Owner ship transferred from lessor to lessee at the end of lease 2. The opening value is equal to the lease liability value. It is worth noting, however, that under, This step-by-step guide covers the basics of lease accounting according to IFRS and, Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to. Even though the new standard does not take effect for public companies until 2019, preparers will want to start assembling the 2017 and 2018 data they will need to present on their 2019 comparative financial statements. The lease term is 3 years while the remaining useful life of the forklift is 5 years. See in EZLease For this office building lease, the journal entries for month twos rent payment would be: To enter this lease in EZLease, follow these steps* : Step 1 Recognize the lease liability and right of use asset In reference to calculation Example 1 from How to Calculate the Lease Liability and Right-of-Use Asset for an Operating Lease under ASC 842, the initial recognition values on 2020-01-01 are: Lease liability $116,357.12 Right of use asset $116,357.12 140 Yonge St. The formula is quite simple you just multiply the annual lease payment by the present value factor, and that results in the net present value of future minimum lease payments, which is recorded on the balance sheet as the lease liability (and ROU asset). For operating leases with a term greater than 12 months, lessees must show a right-of-use asset and a lease liability on their balance sheets, initially recorded at the present value of the lease payments calculated the same way as required for finance leases. At the end of the lease, the equipment will revert to the lessor. Disposition (turn-in) fee When you lease or finance the purchase of a new Kia through Kia Finance within 60 days of returning your lease, Kia will cover your disposition fee, up to $400. var plc456219 = window.plc456219 || 0; In our experience, most LeaseQuery clients have chosen to keep the existing thresholds of 75% and 90%, respectively, for continuity purposes. document.write('

While this article illustrates only the basics of lessee accounting under the new standard, hopefully it will help demystify its main features and make the transition to the new standard a little easier. The first significant effort to cope with lease accounting came in November 1976, when FASB issued Statement of Financial Accounting Standards (SFAS) 13,Accounting for Leases,based on the principle that a lease that transfers substantially all of the benefits and risks incident to the ownership of property should be designated a capital lease and accounted for as the acquisition of an asset and the incurrence of an obligation by the lessee and as a sale or financing by the lessor. Leases not meeting this definition were classified as operating leases, requiring only note disclosure. Financial Modeling & Valuation Analyst (FMVA), Commercial Banking & Credit Analyst (CBCA), Capital Markets & Securities Analyst (CMSA), Certified Business Intelligence & Data Analyst (BIDA), Financial Planning & Wealth Management (FPWM), Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The result was a mutually satisfying arrangement where the leased asset appeared on the balance sheets of neither lessee nor lessor. Discovery of a solution did not take long: Changing lease accounting to reflect the economic reality of lease obligations on lessees financial statements meant overcoming the vested interests of powerful interest groups. Beginning with a Finance Lease, the initial journal entry at transition will resemble this: The amount of the initial measurement of the lease liability, Base Lease: Any Lease Payments at or before the 15th of the month of the Start Date. The two most common types of leases in accounting are operating and finance (or capital) leases. The lease transfers ownership of the underlying asset to the lessee by the end of the lease term. In this article, we'll walk through the initial journal entries for both lease classifications, Finance and Operating at the time of transition. As a refresher, an operating lease functions much like a rental agreement; the lessee pays to use the asset but doesnt enjoy any of the economic benefits nor incur any of the risks of ownership. This is because, for example, a shrewd landlord factors in the future use of the asset when establishing the lease payments, and as such, typically the fourth test would be triggered. The debit to the right-of-use asset is equal to the present value of all remaining lease payments (initial lease liability) PLUS initial direct costs PLUS prepayments LESS any lease incentives. If you would like further information on how to determine the discount rate refer here. There are several inputs when determining the discount rate. If you are unsure if the lease is a partial termination, there is more information here and some practical examples of re-measure the lease liability and right of use asset. The discount rate is the lessors implicit rate or, if not determinable, the lessees incremental borrowing rate for a similar collateralized loan in a similar economic environment. This will be an in-depth calculation example to illustrate how to account for the lease liability and right of use asset to handle any lease permutations, whether that be payments or modifications. The credit to lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year. Payment schedules are more flexible than loan contracts. The difference is subtle, but it has accounting implications. With Example 2, the lease liability amount before modification was $19,885.48. The present value of the sum of lease payments and any residual value guaranteed by the lessee not already reflected in lease payments equals or exceeds substantially all of the fair value of the underlying asset. Criteria 4: Is the present value of the sum of the lease payments substantially all of the fair value of the leased asset? For further information on what inputs can impact the value of the right of use asst refer here. Owner ship transferred from lessor to lessee at the end of lease 2. The opening value is equal to the lease liability value. It is worth noting, however, that under, This step-by-step guide covers the basics of lease accounting according to IFRS and, Whether the risks and rewards have been fully transferred can be unclear, so IFRS outlines several criteria to. Even though the new standard does not take effect for public companies until 2019, preparers will want to start assembling the 2017 and 2018 data they will need to present on their 2019 comparative financial statements. The lease term is 3 years while the remaining useful life of the forklift is 5 years. See in EZLease For this office building lease, the journal entries for month twos rent payment would be: To enter this lease in EZLease, follow these steps* : Step 1 Recognize the lease liability and right of use asset In reference to calculation Example 1 from How to Calculate the Lease Liability and Right-of-Use Asset for an Operating Lease under ASC 842, the initial recognition values on 2020-01-01 are: Lease liability $116,357.12 Right of use asset $116,357.12 140 Yonge St. The formula is quite simple you just multiply the annual lease payment by the present value factor, and that results in the net present value of future minimum lease payments, which is recorded on the balance sheet as the lease liability (and ROU asset). For operating leases with a term greater than 12 months, lessees must show a right-of-use asset and a lease liability on their balance sheets, initially recorded at the present value of the lease payments calculated the same way as required for finance leases. At the end of the lease, the equipment will revert to the lessor. Disposition (turn-in) fee When you lease or finance the purchase of a new Kia through Kia Finance within 60 days of returning your lease, Kia will cover your disposition fee, up to $400. var plc456219 = window.plc456219 || 0; In our experience, most LeaseQuery clients have chosen to keep the existing thresholds of 75% and 90%, respectively, for continuity purposes. document.write(' For more information on this practical expedient, refer here. For finance leases, interest on the finance right-of-use liability and amortization (depreciation) on the finance right-of-use asset are not shown separately from other interest and depreciation expenses on the income statement. For finance and long-term operating leases, the following must be presented on the balance sheet (or disclosed in the footnotes) separately from one another and from other assets and liabilities: Balance Sheet Presentation for Finance and Operating Leases. Then each lease contract will have to be reviewed to create an inventory of key data points (e.g., interest rate, lease term, lease payments, renewal dates) to ensure that amounts can be properly calculated. However, typically, we notice if a lease triggers the fifth test, its likely that it also triggered the third or fourth test. Any required adjustments will need to be done via a journal entry. Web"EZLease maintains all of the lease schedules and we can run custom journal entries out of the system for direct upload into our ERP system. WebStep 1 - Work out the modified future lease payments Step 2 - Determine the appropriate discount rate and re-calculate the lease liability Step 3 - Capture the modification movement and apply that to the ROU asset value Step 4 - Update the right of use asset amortization rate Open site navigation How to Calculate a Finance Lease under ASC 842 2022 The New York State Society of CPAs. These requirements are demonstrated inExhibit 4. It is worth noting, however, that under IFRS, all leases are regarded as finance-type leases. Under ASC 842, the lessee still must perform a lease classification. The two most common types of leases are operating leases and financing leases (also called capital leases). var plc282686 = window.plc282686 || 0; The equipment has a useful life of eight years and has no residual value.

For more information on this practical expedient, refer here. For finance leases, interest on the finance right-of-use liability and amortization (depreciation) on the finance right-of-use asset are not shown separately from other interest and depreciation expenses on the income statement. For finance and long-term operating leases, the following must be presented on the balance sheet (or disclosed in the footnotes) separately from one another and from other assets and liabilities: Balance Sheet Presentation for Finance and Operating Leases. Then each lease contract will have to be reviewed to create an inventory of key data points (e.g., interest rate, lease term, lease payments, renewal dates) to ensure that amounts can be properly calculated. However, typically, we notice if a lease triggers the fifth test, its likely that it also triggered the third or fourth test. Any required adjustments will need to be done via a journal entry. Web"EZLease maintains all of the lease schedules and we can run custom journal entries out of the system for direct upload into our ERP system. WebStep 1 - Work out the modified future lease payments Step 2 - Determine the appropriate discount rate and re-calculate the lease liability Step 3 - Capture the modification movement and apply that to the ROU asset value Step 4 - Update the right of use asset amortization rate Open site navigation How to Calculate a Finance Lease under ASC 842 2022 The New York State Society of CPAs. These requirements are demonstrated inExhibit 4. It is worth noting, however, that under IFRS, all leases are regarded as finance-type leases. Under ASC 842, the lessee still must perform a lease classification. The two most common types of leases are operating leases and financing leases (also called capital leases). var plc282686 = window.plc282686 || 0; The equipment has a useful life of eight years and has no residual value.  var plc461033 = window.plc461033 || 0; For weak-form finance leases (those falling under the other three criterion), the assets are amortized over the shorter of the useful life or the lease term. From a calculation perspective, you also need to remember to update the calculation to use the latest discount rate in the XNPV formula and the calculation of interest earned on the lease liability. A capital lease, now referred to as a finance lease under ASC 842, is a lease with the characteristics of an owned asset. Accounting Entries of Finance and Operating Lease - Accountant Skills Accounting Entries of Finance and Operating Lease September 29, 2018 by Md. [emailprotected]. Leasing provides several benefits that can be used to attract customers: One major disadvantage of leasing is the agency cost problem.

var plc461033 = window.plc461033 || 0; For weak-form finance leases (those falling under the other three criterion), the assets are amortized over the shorter of the useful life or the lease term. From a calculation perspective, you also need to remember to update the calculation to use the latest discount rate in the XNPV formula and the calculation of interest earned on the lease liability. A capital lease, now referred to as a finance lease under ASC 842, is a lease with the characteristics of an owned asset. Accounting Entries of Finance and Operating Lease - Accountant Skills Accounting Entries of Finance and Operating Lease September 29, 2018 by Md. [emailprotected]. Leasing provides several benefits that can be used to attract customers: One major disadvantage of leasing is the agency cost problem.  As a result the calculation will be $28,546.45 / 77 = $370.73.

As a result the calculation will be $28,546.45 / 77 = $370.73.  The equipment under lease had an estimated 5-year useful life with no residual value. So what is the other side of the journal entry? Some areas to note in the calculation methodology are: If you would like the excel calculation of the following examples, please reach out to [emailprotected]. For an operating lease as all cash outflows are classified as "operating" in the statement of cash flows. Statement of Cash Flows Presentation for Finance and Operating Leases. Interest is the additional 3 years is less than 75% of 5 years ( 3.75 years), so the third test for finance lease accounting is not met. On January 1, 2022, Company XYZ signed an eight-year lease agreement for equipment. For operating leases, lease expense will be included among operating expenses. The existing nomenclature of capital lease is no longer specific to one lease type because the majority of leases will now be capitalized (except those with a term of 12 months or less at commencement).

The equipment under lease had an estimated 5-year useful life with no residual value. So what is the other side of the journal entry? Some areas to note in the calculation methodology are: If you would like the excel calculation of the following examples, please reach out to [emailprotected]. For an operating lease as all cash outflows are classified as "operating" in the statement of cash flows. Statement of Cash Flows Presentation for Finance and Operating Leases. Interest is the additional 3 years is less than 75% of 5 years ( 3.75 years), so the third test for finance lease accounting is not met. On January 1, 2022, Company XYZ signed an eight-year lease agreement for equipment. For operating leases, lease expense will be included among operating expenses. The existing nomenclature of capital lease is no longer specific to one lease type because the majority of leases will now be capitalized (except those with a term of 12 months or less at commencement).  Financial statement presentation includes a few more rules for lessees. XYZ Ltd. charges a total of $1,500 in the lease transaction. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. In contrast to ASC 840, under ASC 842, the existence of a purchase option does not automatically classify a lease arrangement as a finance lease. AdButler.ads.push({handler: function(opt){ AdButler.register(165519, 461033, [300,600], 'placement_461033_'+opt.place, opt); }, opt: { place: plc461033++, keywords: abkw, domain: 'servedbyadbutler.com', click:'CLICK_MACRO_PLACEHOLDER' }}); The beginning journal entry records the fair market value of the digger (as PPE), and the depreciation journal entry splits the fair market value by the cost of annual use. (function(){ The amortization for a finance lease under ASC 842 is very straightforward. Interestingly, this added criterion was previously considered for inclusion in SFAS 13, but was rejected because it was considered too difficult to objectively define. (function(){ For finance leases that transfer ownership at the end of the lease term or for those that contain a lease purchase option, I.e. In this example, the right of use asset value is 116,375.00. var AdButler = AdButler || {}; AdButler.ads = AdButler.ads || []; As a result, this lease is classified as a finance lease per the fourth test. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. In this case, its 2021-1-1 to 2021-12-31. Structured Query Language (known as SQL) is a programming language used to interact with a database. Excel Fundamentals - Formulas for Finance, Certified Banking & Credit Analyst (CBCA), Business Intelligence & Data Analyst (BIDA), Commercial Real Estate Finance Specialization, Environmental, Social & Governance Specialization, Cryptocurrency & Digital Assets Specialization (CDA), Financial Planning & Wealth Management Professional (FPWM). The finance lease accounting journal entries below act as a quick reference, and set out the most commonly encountered situations when dealing with the double entry posting of finance or capital leases. Simply excluding transfer and purchase features from a lease could circumvent the first two criteria, and the bright lines of the remaining two criteria were sidestepped with terms, interest rates, and other stipulations engineered to stay below the 75% and 90% thresholds. document.write('

Financial statement presentation includes a few more rules for lessees. XYZ Ltd. charges a total of $1,500 in the lease transaction. This step-by-step guide covers the basics of lease accounting according to IFRS and US GAAP. In contrast to ASC 840, under ASC 842, the existence of a purchase option does not automatically classify a lease arrangement as a finance lease. AdButler.ads.push({handler: function(opt){ AdButler.register(165519, 461033, [300,600], 'placement_461033_'+opt.place, opt); }, opt: { place: plc461033++, keywords: abkw, domain: 'servedbyadbutler.com', click:'CLICK_MACRO_PLACEHOLDER' }}); The beginning journal entry records the fair market value of the digger (as PPE), and the depreciation journal entry splits the fair market value by the cost of annual use. (function(){ The amortization for a finance lease under ASC 842 is very straightforward. Interestingly, this added criterion was previously considered for inclusion in SFAS 13, but was rejected because it was considered too difficult to objectively define. (function(){ For finance leases that transfer ownership at the end of the lease term or for those that contain a lease purchase option, I.e. In this example, the right of use asset value is 116,375.00. var AdButler = AdButler || {}; AdButler.ads = AdButler.ads || []; As a result, this lease is classified as a finance lease per the fourth test. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. In this case, its 2021-1-1 to 2021-12-31. Structured Query Language (known as SQL) is a programming language used to interact with a database. Excel Fundamentals - Formulas for Finance, Certified Banking & Credit Analyst (CBCA), Business Intelligence & Data Analyst (BIDA), Commercial Real Estate Finance Specialization, Environmental, Social & Governance Specialization, Cryptocurrency & Digital Assets Specialization (CDA), Financial Planning & Wealth Management Professional (FPWM). The finance lease accounting journal entries below act as a quick reference, and set out the most commonly encountered situations when dealing with the double entry posting of finance or capital leases. Simply excluding transfer and purchase features from a lease could circumvent the first two criteria, and the bright lines of the remaining two criteria were sidestepped with terms, interest rates, and other stipulations engineered to stay below the 75% and 90% thresholds. document.write('