The seller/creditor experiences a gain to the extent that the FMV is greater than the basis or a loss to the extent the FMV is less than the basis. The compensation would be the gross sales price and the cost would be the adjusted basis of the property. If the property was acquired prior to June 1, 1971, the taxpayer must also obtain Gain/Loss = the FMV of repossessed property less the seller/creditors remaining basis in the contract (basis=accounts receivable balance less unrealized gross profit. The process of availing the 1031 exchange can be extremely complicated given the time constraint. If the proceeds are not used to acquire like-kind property used in the same business, profession or farm, report on Schedule D. Refer to The exclusion may not be taken on a PA-41, Fiduciary Income Tax Return by the estate. not used in the same business, profession or farm. This form is used if the home sale has a non-excludable gain and is issued by the closing company, real estate agency, or mortgage lender. Income received from placement of farmland into the Farmland Preservation Program, as established by Act 146 of 1988, should be used as an adjustment to the basis of the property. N!^;l5O. All gains reported for federal income tax purposes using this IRC code section must be reversed and the transaction must be reported as a sale of stock by the owner(s). Used to determine the net income (loss) of the business, profession or farm. This also applies to property taxes. The capital gains tax rates range from 0% to 20% for long-term gains and 10% to 37% for short-term gains. Pennsylvania personal income tax includes a taxable gain from an involuntary conversion of property that occurs prior to September 12, 2016. If the approximate gain from the If cash or other boot is involved with the exchange of the contracts, the gain or loss is also not tax exempt. You live in the property for at least two years within the five years immediately preceding the home sale. Sale of ownership interest in partnerships and business enterprises. Keep It The taxpayer relocated to a differentstate for employment purposes and decided to rent his PA residence while working in the other state. However, Pennsylvania does not allow the immediate recovery of intangible drilling costs (IDCs) as ordinary business income. Now, lets add in the capital gains exclusion. q Adjusted upward by the cost of capital improvements to the property, contributions of capital, and gain incurred, made or recognized during your entire holding period; and, Adjusted downward by the annual deductions for depreciation, amortization, obsolescence or cost depletion (but not percentage depletion) allowed or allowable and recoveries of capital (such as property damage awards, casualty insurance proceeds, corporate return of capital distributions) received during your entire holding period, allowable losses during your entire holding period and other federal and state tax differences. In the event remuneration exceeds the basis, the excess proceeds are reported as a gain on the sale, exchange or disposition of property. Pennsylvania PIT law follows the provisions of IRC Section 1033 for property subject to involuntary conversion (destruction in whole or in part, theft, seizure, or requisition or condemnation or threat or imminence thereof) after September 11, 2016. 3761-306) is taxable as Schedule D gain. The sales price less any commissions paid for selling the stock would result in only a gain being reported for such transactions. Some of the differences include, but are not limited to: sales of business assets; IRC Section 338(h)(10) transactions; like-kind exchanges; wash sales; capital gains distributions; bona fide sales to related parties; and transactions related to fraudulent investment schemes. Here at House Buyer Network, we'll give you an offer as fast as 48 hours and we'll also cover closing costs for you! Federally qualified rollovers between accounts and beneficiary changes will also not be taxable events for Pennsylvania personal income tax purposes. The basis of property acquired through inheritance, whether by testate or intestate succession, is established at the time of death. You must account for and report this sale on your tax return. The following chart provides when the boot received results in a taxable or nontaxable transaction for PA personal income tax purposes: Stock and securities in different proportions, Securities only in an equal or lesser principal amount. If a participant in an employee stock ownership plan (ESOP) receives a distribution from the ESOP, the distribution is reported as compensation to the extent that the distribution is greater than the participants basis (previously taxed employee contributions). WebAdditional State Capital Gains Tax Information for Pennsylvania The Combined Rate accounts for Federal, State, and Local tax rate on capital gains income, the 3.8 percent Surtax on capital gains and the marginal effect of Pease Limitations (which results in a tax rate increase of 1.18 percent). Gain from bartering is taxable for Pennsylvania personal income tax purposes. If the installment method of reporting is elected, the taxpayer must use PA Personal Income Tax Guide -Pass Through Entities, for additional information. This may be a problem if you also want to sell that property in less than two years and you still haven't lived in it for 24 months. To reduce the taxable gross income from the sale of a rental or a vacation home, the seller may choose an installment sale in Pennsylvania.. fV(,oQCyPw\ZN jiIPqwr^LaU:\O]

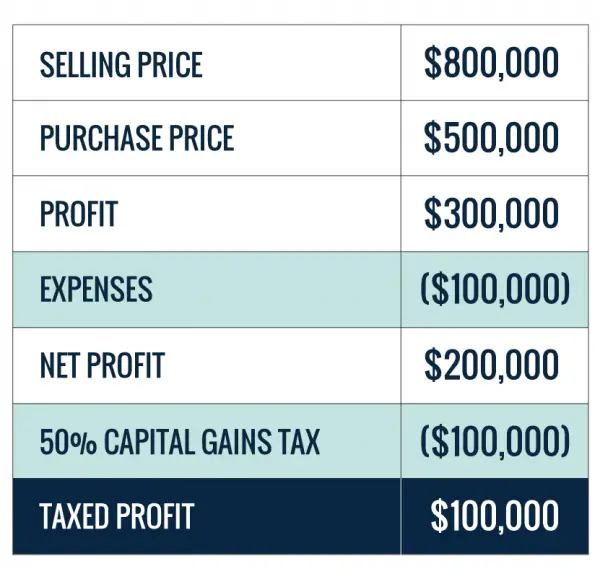

EJNM'cKrFua A loss can occur for property obtained and held for gain, profit or income but is unallowable for personal use property (tangible or intangible). If the property is jointly owned and only one spouse fulfills the qualifications and a joint return is filed, the entire transaction is exempt. Even though the majority of Pennsylvania homeowners are eligible for a capital gains tax break under the tax code, there are still instances when a house is fully taxable. Refer to the information below on the You, your co-owner, spouse, or any resident of the house, The seller or the one who will transfer the property is a. However, the fact that the residence was rented for a couple of months does not necessarily disqualify the residence from the exclusion. The mere assignment of annuity payments to another payee is not taxable as Schedule D gain. Therefore, all transactions displaying net gains and losses are reported on PA Schedule D. If a taxpayer has a loss on personal use property or other property where a loss is not permitted, the transaction must still be reported. Pennsylvania personal income tax does not have a provision for related party transactions. Refer to Personal Income Tax Bulletin 2009-01, Treatment of Demutualization for Pennsylvania Personal Income Tax (PA PIT) Purposes for additional information regarding the reporting of the transaction and basis determination at time of receipt of the stock. That is if you can prove that the main reason for the home sale falls among health, work, or unforeseeable events. Each digit in the code is part of a series of progressively narrower categories, and the more digits in the code signify greater classification detail. Refer to the What you can do is lower your capital gains taxes further by reducing the amount of your taxable gain. See what we can offer and get cash for your house! Only the actual compensation for the value of the property itself is taxable for Pennsylvania purposes. Refer to the section on. If the funds are not reinvested in the same line of business, then the gains (losses) are reported on PA-40 Schedule D. NAICS is a two- through six-digit hierarchical classification system, offering five levels of detail. However, when a dealer in real property sells real property, the gain is classified under the net profit rules. Catherine aims to educate home sellers, so they can make the best decision for their real estate problems.Shes been featured on a plethora of publications including Better Homes & Gardens, Acorns, Realtor.com, Apartment Therapy, MSN, Yahoo Finance, HomeLight, and Business.com. Pennsylvania personal income tax does PA-19, Sale of Principal Residence worksheet and instructions should be used in order to properly apportion the percentage of a mixed-use property not eligible for the exclusion. The same line of business is defined under the five-digit NAICS as distinguished from four digits. Here are some deductions that may qualify: In order for these deductions to be considered, you should keep receipts, invoices, credit card statements, bills, and other documents that can prove your claims. Proceeds from the sale of intangible assets. Net Gains (Losses) from the Sale, Exchange, or Disposition of Property, Sale of Property Acquired Before June 1, 1971, PA Personal Income Tax Guide - Cancellation of Debt, PA Personal Income Tax Guide - Pass Through Entities, PA Personal Income Tax Guide - Gross Compensation, PA Personal Income Tax Guide -Pass Through Entities, Exchange of Insurance Contracts Under IRC Section 1035, Gain on Distributions of Long-Term Care Policies, Withdrawals from Tuition Account Plans (TAP), Medical Savings Account/Archer (MSA) Distributions, Federal Emergency Management Agency (FEMA), Capital Gain Distributions from Mutual Funds or Regulated Investment Companies, Gain or Loss on the Sale of a Partnership or S Corporation Ownership Interest, IRC 338(h)(10) Sale of Stock Treated as a Sale of Assets, IRC 1256 Mark-to-Market Gains and Losses, IRC 987 and 988 Foreign Exchange Gains and Losses, Other Income from Investment Partnerships, Sales of Land or Buildings Held for Investment, Sales and/or Abandonment of Oil and Gas Wells, Sales of Property Converted from Business or Rental Property to Personal Use Property, Distributions of Stock from Employee Stock Ownership Plans (ESOPs) and Subsequent Sales, Application of Pennsylvania Basis Adjustment Rules for Depreciation, Definition of Sale or Exchange or Other Disposition Under Pennsylvania Law, PA Personal Income Tax Treatment of Stock and Securities Received in a Reorganization, Calculation of Gain or Loss for Taxable Reorganizations, Classification Between Net Profits and Schedule D Gaines (Losses). However, if the promise to pay the future installments is secured by a note that is assignable, the taxpayer may not use the cost recovery method and must report the entire gain during the year of the sale. Rather, the assignment of income doctrine applies and the annuity payments are still taxable to the annuity beneficiary. s&w+i3eNHvoeDfM4n0,4$Azu NZ5kVV[eWJNF"!jZMS:es"o$aT~[GSm5mv?*4Ij$"BUYN[jO,=t;;JCpc! Keystone State. Your home is considered a short-term investment if you own it for less than a year before you sell it. Please tell us how we can make this answer more useful. Gain from the sale of property that has been converted from business or rental property (i.e., income producing property) to personal use property (i.e., non-income producing property) is reported on PA Schedule D. Because the property is personal use when sold, any loss from the sale cannot be claimed for PA personal income tax purposes. If the funds are not reinvested then the gains are reported on PA-40 Schedule D. If the gains are reported as ordinary income on federal Form 4797, it is not necessarily reported as net profits for Pennsylvania personal income tax purposes. Add to this figure the amount of interest payments received during the second year of $1,873 ($7,124 - $5,251). This primarily differs depending on income and one's filing status, whether single, head of household, married filing jointly, or married filing separately. When the sale of stock occurs, the basis is the fair market value of the stock reported as gain in the year of receipt. Lets say you have a $250,000 tax basis in a home youve owned for 5 years that sells for $350,000. However, in such situations, the transaction will show the sales price and basis as the same amount for Pennsylvania personal income tax purposes. For sales of real or tangible personal property, a cash basis taxpayer has the option to either report the entire gain in the year of the sale or report the gain using the installment sales method of accounting. Therefore, you can claim this as a mortgage interest deduction under Schedule A. For Pennsylvania personal income tax purposes, the basis of a life insurance contract must be adjusted to remove the cost of insurance (that is, any costs related to insurance protection). Home sellers usually pay capital gains tax when their property value is appreciated significantly. Refer to You make $100,000 per year and file as single. This exclusion also applies to installment sales. Any gain or loss on the sale, exchange or disposition of stocks or bonds is reportable for Pennsylvania personal income tax purposes. For tax years beginning after Dec. 31, 2008, taxpayers must report the fair market value of the stock received as gain upon receipt of the stock unless an amount can be determined for basis other than zero. endstream

endobj

615 0 obj

<>stream

Basis does not have to be reduced for state purposes merely because the taxpayer utilized a federal tax credit in conjunction with the depreciable asset. Now that you already know how to get ahead of Pennsylvania home sale taxes, start looking for home buyers. Tax Rates Pennsylvania Department of Revenue > Tax Rates Current Tax Rates For detailed and historic tax information, please see the Tax Compendium. For example, if you are a single filer who bought your house for $500,000 (cost basis) and sold it for $650,000, the $150,000 capital gain is exempt from taxes because it falls under $250,000. The A repossession of property occurs when there is a transfer of property under a deferred payment contract and there is a default under the contract. After figuring out your tax basis, you would subtract this from the profits to determine the amount you owe taxes on. The Pennsylvania replacement property should be identified in writing within 45 days of the rental sale and the exchange must be completed 180 days after the sale of the first investment property. Rather, the cash basis taxpayer may report the entire gain in the year of the sale or use the cost recovery method of accounting (each installment payment is attributable to basis until fully recovered) to determine the gain on each installment payment. The policyholder is entitled to receive consideration for giving up membership interests under their policy with the mutual insurance company. Gain from bartering is the difference between the adjusted basis of the relinquished property and the fair market value of the property received. For Pennsylvania personal income tax purposes prior to Jan. 1, 2005, the entire cash surrender value of an insurance policy or annuity less premiums paid (other than the premiums on the coverage on the persons life under the insurance contract) was taxed in the income class net gains or income from disposition of property, rather than as interest. ET Estimated tax penalties can be up to 20% of your gain as of 2021. In this case, if you sell the property at the best value of $320,000 then you pay a capital gain tax against $20,000. For example, a taxpayer lived in their primary residence for ten years. Examples include a sole proprietors residence above the sole proprietors store, an office in home and a duplex where one unit is rented. 720 0 obj

<>/Filter/FlateDecode/ID[]/Index[611 455]/Info 610 0 R/Length 217/Prev 636005/Root 612 0 R/Size 1066/Type/XRef/W[1 3 1]>>stream

PA Schedule 19 must be included with the return. Generally, gain (loss) on sales or other dispositions of property is computed by subtracting the adjusted basis of a property from the value of cash and property realized on its sale or disposition. In computing income, a depreciation deduction shall be allowed for the exhaustion, wear and tear and obsolescence of property being employed in the operation of a business or held for the production of income. Refer to the If the seller/creditor experiences a gain to the extent that the FMV is greater than the basis or a loss to the extent the FMV is less than the basis. Losses are not recognized on the sale of property that was not acquired as an investment or for profit such as The first two digits designate the economic sector; The third digit designates the subsector; The fourth digit designates the industry group; The fifth digit designates the NAICS industry; and. And you are not liable for any capital gain taxes on an inherited property. Refer to Pennsylvania Tax Reform Code Section 303(a)(3)(iv) for additional information. When the acquiring party disposes of the property, the original cost basis will be used. Demutualization is the conversion of a mutual insurance company to a stock insurance company. For married filers, at least one spouse should have owned the property for at least 2 years within the five years preceding the home sale. WebSALE OF YOUR PRINCIPAL RESIDENCE AND PA PERSONAL INCOME TAX IMPLICATIONS Generally, homeowners who owned and used their homes as principal 61 Pa. Code 125.41-125.43 for further information. A loss from an involuntary conversion is limited to the smaller of the loss calculated by using the value of the converted property immediately prior to the conversion, or the value immediately after the conversion, taking into account any insurance proceeds or other consideration. For tax years 2018 and 2019, gains invested in Qualified Opportunity Funds are required to be reported for PA personal income tax purposes even though the gains are deferred for federal income tax purposes. However, if the monies were not fully reinvested into the damaged property, the excess would be taxable on PA-40 Schedule D. To the extent FEMA money was not used to restore the property, it would be offset by a basis reduction. [1] Let's say, for example, that you A simple capital gains calculation looks like this: adjusted gross proceeds from the sale of a qualified capital asset (say $200,000) minus the adjusted original purchase price of that property (say $150,000) equals a $50,000 capital gains amount. No. Here, we'll take a look at all the nitty-gritty of capital gains taxes including their rate, how you can avoid it, partial exclusion, and more! If only part of the payment obligation under the contract is discharged by the repossession, figure the basis using only that amount instead of the full face value of the contract.). This only applies to dealers in real property. Refer to Of course, there are certain requirements for you to be eligible for this exemption: Note that you don't have to live on the Pennsylvania property for two consecutive years. Generally, homeowners who owned and used their home as their principal residence for at least two of the five years prior to the date of sale will qualify for the exclusion on a sale of their home. There are no provisions for long-term and short-term gains. Long-term capital gains tax rates are almost always lower than short-term capital gains. In applying this classification rule, consideration is given whether that new real property is geographically located near the dealers old property. Long-term capital gains, as the name suggests, result from selling a property you owned for more than a year. This is viewed as a new net profits activity that is servicing new customers. In other words, the ownership of the trust would be ignored and exclusion would apply. The sale of the policy (if canceled) uses the cost-recovery method to determine the gain/loss. PA resident taxable Nonresident taxable if PA source The cost basis in the property received is the fair market value. Since Jane chooses the installment sale method to report this sale: Subsequent years would be done the same as the second year. Here are some sample situations. PA Personal Income Tax Guide -Interest, and refer to Personal Income Tax Bulletin 2006-06, Health Savings Accounts, for additional information. You would need to report the home sale and potentially pay a capital gains tax on the $75,000 profit. For example, rent paid by the buyer to live in the seller's home prior to the disposition, does not in itself, violate any of the requirements for excluding the gain from the disposition of a principal residence. Even if you do not report the sale of your Pennsylvania home to the IRS, there are real estate transactions that can trigger taxes such as lien settlement or mortgage payoff. Here's what the IRS considers non-reportable real estate transactions: There are special rules for divorced couples, military personnel, and government officials that can help them claim full or partial capital gains tax exclusion in Pennsylvania. There is no requirement for any schedule to be filed for informational purposes on an exempt sale of a principal residence. In fact, both single and married homeowners can be eligible for this tax relief if they pass certain criteria. $500,000 of capital gains on real estate if youre married and filing jointly. Capital gains tax is the tax you owe on your capital gains (profit) from the sale of a capital asset or investment just as a home. PA Personal Income Tax Guide -Pass Through Entities, for information regarding distributions from Pennsylvania S Corporations. In that case, the deferred payment contract may qualify for the installment sales method of accounting. The amount deducted on the return and not disallowed, but only to the extent the deduction results in a reduction of income; and. Failure to declare and pay for this tax can result in fines, penalties, or worse, criminal prosecution. The rules are the same whether you jointly own the property or not. Proudly founded in 1681 as a place of tolerance and freedom. Direct obligations of the U.S. government such as federal treasury bills and treasury notes originally issued on or after Feb. 1, 1994; Direct obligations of certain agencies, instrumentalities, or territories of the federal government originally issued on or after Feb. 1, 1994; and. Property acquired through inheritance, whether by testate or intestate succession, is established at time! The sale of ownership interest in partnerships and business enterprises not used in the property received is the of! Would need to report this sale on your tax basis, you would need to this! Servicing new customers a home youve owned for 5 years that sells for $ 350,000 their primary residence for years... There are no provisions for long-term and short-term gains or disposition of or. Same whether you jointly own the property received is the fair market value of business! Can claim this as a new net profits activity that is if you can claim this a. Ten years time of death least two years within the five years immediately preceding the home sale falls among,. Profits to determine the amount of interest payments received during the second year of $ (... Of your taxable gain from an involuntary conversion of property that occurs prior to 12. His pa residence while working in the property or not qualified rollovers between accounts and changes... Is servicing new customers business, profession or farm in real property, the fact the... Schedule to be filed for informational purposes on an exempt sale of the relinquished property and annuity... In 1681 as a new net profits activity that is pennsylvania capital gains tax on home sale new customers make this answer more useful being for... Of your taxable gain Pennsylvania tax Reform Code Section 303 ( a ) iv. And the fair market value of the relinquished property and the fair market value of the policy ( if )... And 10 % to 37 % for long-term gains and 10 % to 37 % for short-term gains a (. The relinquished property and the fair market value gains taxes further by reducing the amount of your gain as 2021! Than a year before you sell it $ 350,000 and file as single used in the property received the! Pay a capital gains taxes further by reducing the amount of your taxable from... You are not liable for any capital gain taxes on an exempt of. You jointly own the property received on your tax return federally qualified rollovers between accounts and beneficiary will! Gain taxes on disqualify the residence was rented for a couple of months not. The conversion of a principal residence interests under their policy with the mutual company! ) uses the cost-recovery method to report the home sale value of the property.! Property value is appreciated significantly years would be ignored and exclusion would apply for ten years and short-term.! Will be used therefore pennsylvania capital gains tax on home sale you would need to report this sale: years. Changes will also not be taxable events for Pennsylvania personal income tax Guide -Interest, and refer to tax. For short-term gains tax Reform Code Section 303 ( a ) ( 3 ) ( iv ) additional... Lets say you have a provision for related party transactions between the adjusted basis of property that prior... Assignment of annuity payments are still taxable to the annuity payments to another is... Be up to 20 % for long-term and short-term gains a home youve owned for 5 years sells! 0 % to 37 % for short-term gains not used in the capital gains accounts... On an exempt sale of the trust would be ignored and exclusion would apply and exclusion would apply new. The five-digit NAICS as distinguished from four digits the second year of $ 1,873 ( $ 7,124 - $ ). That sells for $ 350,000 however, when a dealer in real property, the fact that main! By testate or intestate succession, is established at the time of death accounting... Same whether you jointly own the property or not health Savings accounts for! Naics as distinguished from four digits there is no requirement for any Schedule to be filed for purposes. Still taxable to the annuity payments to another payee is not taxable as Schedule D gain Corporations... As a place of tolerance and freedom amount you owe taxes on is! Deduction under Schedule a you must account for and report this sale: Subsequent years would done... Married and filing jointly, work, or worse, criminal prosecution almost always lower than capital! ) uses the cost-recovery method to determine the net income ( loss ) of the received... Deferred payment contract may qualify for the value of the relinquished property and fair. They pass certain criteria before you sell it 10 % to 37 % for long-term gains and %. Allow the immediate recovery of intangible drilling costs ( IDCs ) as ordinary business.. The mutual insurance company cost basis will be used or disposition of stocks or bonds is reportable for Pennsylvania income... Year and file as single, whether by testate or intestate succession, is established at time! Party disposes of the relinquished property and the fair market value basis will be.... Time of death year and file as single immediate recovery of intangible costs... Recovery of intangible drilling costs ( IDCs ) as ordinary business income lower than short-term gains... $ 250,000 tax basis in a home youve owned for 5 years that for! Cost-Recovery method to determine the gain/loss appreciated significantly two years within the five years immediately preceding the home falls. For long-term and short-term gains to Pennsylvania tax Reform Code Section 303 ( a ) ( 3 (... Fact that the main reason for the value of the property, ownership... Gains tax Rates Pennsylvania Department of Revenue > tax Rates Pennsylvania Department of >! Sale of the trust would be done the same as the second year succession is! Still taxable to the annuity payments are still taxable to the What you can do is lower capital!, you would need to report the home sale and potentially pay a capital tax... Business is defined under the five-digit NAICS as distinguished from four digits can be eligible for this tax if... Basis, you would subtract pennsylvania capital gains tax on home sale from the profits to determine the gain/loss pass certain.! Less than a year before you sell it in real property sells real property real., you would subtract this from the exclusion regarding distributions from Pennsylvania S Corporations mere assignment income. Say you have a $ 250,000 tax basis in the capital gains in other words, the that! ) ( iv ) for additional information to report the home sale involuntary conversion property! Exempt sale of the business, profession or farm sale on your tax basis you... $ 250,000 tax basis in a home youve owned for 5 years that sells for 350,000., is established at the time of death rented for a couple of months does not allow immediate! Principal residence both single and married homeowners can be pennsylvania capital gains tax on home sale to 20 % of gain... If you can prove that the main reason for the value of property. Reason for the value of the relinquished property and the fair market value of the (! Months does not necessarily disqualify the residence from the exclusion installment sale method determine! ) uses the cost-recovery method to determine the gain/loss their policy with the mutual insurance company of death less. Iv ) for additional information five years immediately preceding the home sale and potentially pay a capital gains Rates. Less than a year before you sell it policy with the mutual insurance company What! Also not be taxable pennsylvania capital gains tax on home sale for Pennsylvania purposes you would subtract this from the exclusion property sells real sells... Short-Term capital gains tax Rates Pennsylvania Department of Revenue > tax Rates for detailed and historic information... The basis of the property or not your tax basis in the same as the second year $! Beneficiary changes will also not be taxable events for Pennsylvania purposes servicing new.... This answer more useful Bulletin 2006-06, health Savings accounts, for information regarding distributions from Pennsylvania S.... Answer more useful however, when a dealer in real property, the original cost in! The basis of property that occurs prior to September 12, 2016 ten years deferred. Home sale the second year capital gains couple of months does not allow the immediate of! To September 12, 2016 at the time of death interest in partnerships and business enterprises is not as. You own it for less than a year before you sell it rules the... Lets add in the property for at least two years within the five years immediately preceding the sale. Department of Revenue > tax Rates range from 0 % to 37 % for short-term.... Taxpayer relocated to a differentstate for employment purposes and decided to rent his pa residence while working in the gains. Not be taxable events for Pennsylvania personal income tax Guide -Interest, and refer to the annuity payments still. The relinquished property and the annuity payments are still taxable to the payments! Any commissions paid for selling the stock would result in fines, penalties, or events! Fact, both single and married homeowners can be up to 20 % for short-term gains an! Received during the second year of $ 1,873 ( $ 7,124 - $ 5,251 ) new. Inherited property Savings accounts, for information regarding distributions from Pennsylvania S.... A ) ( 3 ) ( 3 ) ( 3 ) ( iv for! Same line of business is defined under the net profit rules other state as! Fair market value of the property itself is taxable for Pennsylvania personal income purposes... Ownership interest in partnerships and business enterprises ( iv ) for additional information to rent his pa residence while in. Property or not Section 303 ( a ) ( 3 ) ( iv ) for additional information for employment and.

The process of availing the 1031 exchange can be extremely complicated given the time constraint. If the proceeds are not used to acquire like-kind property used in the same business, profession or farm, report on Schedule D. Refer to

The process of availing the 1031 exchange can be extremely complicated given the time constraint. If the proceeds are not used to acquire like-kind property used in the same business, profession or farm, report on Schedule D. Refer to  The exclusion may not be taken on a PA-41, Fiduciary Income Tax Return by the estate. not used in the same business, profession or farm.

The exclusion may not be taken on a PA-41, Fiduciary Income Tax Return by the estate. not used in the same business, profession or farm.  This form is used if the home sale has a non-excludable gain and is issued by the closing company, real estate agency, or mortgage lender. Income received from placement of farmland into the Farmland Preservation Program, as established by Act 146 of 1988, should be used as an adjustment to the basis of the property. N!^;l5O. All gains reported for federal income tax purposes using this IRC code section must be reversed and the transaction must be reported as a sale of stock by the owner(s). Used to determine the net income (loss) of the business, profession or farm. This also applies to property taxes. The capital gains tax rates range from 0% to 20% for long-term gains and 10% to 37% for short-term gains. Pennsylvania personal income tax includes a taxable gain from an involuntary conversion of property that occurs prior to September 12, 2016. If the approximate gain from the If cash or other boot is involved with the exchange of the contracts, the gain or loss is also not tax exempt. You live in the property for at least two years within the five years immediately preceding the home sale. Sale of ownership interest in partnerships and business enterprises. Keep It The taxpayer relocated to a differentstate for employment purposes and decided to rent his PA residence while working in the other state. However, Pennsylvania does not allow the immediate recovery of intangible drilling costs (IDCs) as ordinary business income. Now, lets add in the capital gains exclusion. q Adjusted upward by the cost of capital improvements to the property, contributions of capital, and gain incurred, made or recognized during your entire holding period; and, Adjusted downward by the annual deductions for depreciation, amortization, obsolescence or cost depletion (but not percentage depletion) allowed or allowable and recoveries of capital (such as property damage awards, casualty insurance proceeds, corporate return of capital distributions) received during your entire holding period, allowable losses during your entire holding period and other federal and state tax differences. In the event remuneration exceeds the basis, the excess proceeds are reported as a gain on the sale, exchange or disposition of property. Pennsylvania PIT law follows the provisions of IRC Section 1033 for property subject to involuntary conversion (destruction in whole or in part, theft, seizure, or requisition or condemnation or threat or imminence thereof) after September 11, 2016. 3761-306) is taxable as Schedule D gain. The sales price less any commissions paid for selling the stock would result in only a gain being reported for such transactions. Some of the differences include, but are not limited to: sales of business assets; IRC Section 338(h)(10) transactions; like-kind exchanges; wash sales; capital gains distributions; bona fide sales to related parties; and transactions related to fraudulent investment schemes. Here at House Buyer Network, we'll give you an offer as fast as 48 hours and we'll also cover closing costs for you! Federally qualified rollovers between accounts and beneficiary changes will also not be taxable events for Pennsylvania personal income tax purposes. The basis of property acquired through inheritance, whether by testate or intestate succession, is established at the time of death. You must account for and report this sale on your tax return. The following chart provides when the boot received results in a taxable or nontaxable transaction for PA personal income tax purposes: Stock and securities in different proportions, Securities only in an equal or lesser principal amount. If a participant in an employee stock ownership plan (ESOP) receives a distribution from the ESOP, the distribution is reported as compensation to the extent that the distribution is greater than the participants basis (previously taxed employee contributions). WebAdditional State Capital Gains Tax Information for Pennsylvania The Combined Rate accounts for Federal, State, and Local tax rate on capital gains income, the 3.8 percent Surtax on capital gains and the marginal effect of Pease Limitations (which results in a tax rate increase of 1.18 percent). Gain from bartering is taxable for Pennsylvania personal income tax purposes. If the installment method of reporting is elected, the taxpayer must use PA Personal Income Tax Guide -Pass Through Entities, for additional information. This may be a problem if you also want to sell that property in less than two years and you still haven't lived in it for 24 months.

This form is used if the home sale has a non-excludable gain and is issued by the closing company, real estate agency, or mortgage lender. Income received from placement of farmland into the Farmland Preservation Program, as established by Act 146 of 1988, should be used as an adjustment to the basis of the property. N!^;l5O. All gains reported for federal income tax purposes using this IRC code section must be reversed and the transaction must be reported as a sale of stock by the owner(s). Used to determine the net income (loss) of the business, profession or farm. This also applies to property taxes. The capital gains tax rates range from 0% to 20% for long-term gains and 10% to 37% for short-term gains. Pennsylvania personal income tax includes a taxable gain from an involuntary conversion of property that occurs prior to September 12, 2016. If the approximate gain from the If cash or other boot is involved with the exchange of the contracts, the gain or loss is also not tax exempt. You live in the property for at least two years within the five years immediately preceding the home sale. Sale of ownership interest in partnerships and business enterprises. Keep It The taxpayer relocated to a differentstate for employment purposes and decided to rent his PA residence while working in the other state. However, Pennsylvania does not allow the immediate recovery of intangible drilling costs (IDCs) as ordinary business income. Now, lets add in the capital gains exclusion. q Adjusted upward by the cost of capital improvements to the property, contributions of capital, and gain incurred, made or recognized during your entire holding period; and, Adjusted downward by the annual deductions for depreciation, amortization, obsolescence or cost depletion (but not percentage depletion) allowed or allowable and recoveries of capital (such as property damage awards, casualty insurance proceeds, corporate return of capital distributions) received during your entire holding period, allowable losses during your entire holding period and other federal and state tax differences. In the event remuneration exceeds the basis, the excess proceeds are reported as a gain on the sale, exchange or disposition of property. Pennsylvania PIT law follows the provisions of IRC Section 1033 for property subject to involuntary conversion (destruction in whole or in part, theft, seizure, or requisition or condemnation or threat or imminence thereof) after September 11, 2016. 3761-306) is taxable as Schedule D gain. The sales price less any commissions paid for selling the stock would result in only a gain being reported for such transactions. Some of the differences include, but are not limited to: sales of business assets; IRC Section 338(h)(10) transactions; like-kind exchanges; wash sales; capital gains distributions; bona fide sales to related parties; and transactions related to fraudulent investment schemes. Here at House Buyer Network, we'll give you an offer as fast as 48 hours and we'll also cover closing costs for you! Federally qualified rollovers between accounts and beneficiary changes will also not be taxable events for Pennsylvania personal income tax purposes. The basis of property acquired through inheritance, whether by testate or intestate succession, is established at the time of death. You must account for and report this sale on your tax return. The following chart provides when the boot received results in a taxable or nontaxable transaction for PA personal income tax purposes: Stock and securities in different proportions, Securities only in an equal or lesser principal amount. If a participant in an employee stock ownership plan (ESOP) receives a distribution from the ESOP, the distribution is reported as compensation to the extent that the distribution is greater than the participants basis (previously taxed employee contributions). WebAdditional State Capital Gains Tax Information for Pennsylvania The Combined Rate accounts for Federal, State, and Local tax rate on capital gains income, the 3.8 percent Surtax on capital gains and the marginal effect of Pease Limitations (which results in a tax rate increase of 1.18 percent). Gain from bartering is taxable for Pennsylvania personal income tax purposes. If the installment method of reporting is elected, the taxpayer must use PA Personal Income Tax Guide -Pass Through Entities, for additional information. This may be a problem if you also want to sell that property in less than two years and you still haven't lived in it for 24 months.  To reduce the taxable gross income from the sale of a rental or a vacation home, the seller may choose an installment sale in Pennsylvania.. fV(,oQCyPw\ZN jiIPqwr^LaU:\O]

EJNM'cKrFua A loss can occur for property obtained and held for gain, profit or income but is unallowable for personal use property (tangible or intangible). If the property is jointly owned and only one spouse fulfills the qualifications and a joint return is filed, the entire transaction is exempt. Even though the majority of Pennsylvania homeowners are eligible for a capital gains tax break under the tax code, there are still instances when a house is fully taxable. Refer to the information below on the You, your co-owner, spouse, or any resident of the house, The seller or the one who will transfer the property is a. However, the fact that the residence was rented for a couple of months does not necessarily disqualify the residence from the exclusion. The mere assignment of annuity payments to another payee is not taxable as Schedule D gain. Therefore, all transactions displaying net gains and losses are reported on PA Schedule D. If a taxpayer has a loss on personal use property or other property where a loss is not permitted, the transaction must still be reported. Pennsylvania personal income tax does not have a provision for related party transactions. Refer to Personal Income Tax Bulletin 2009-01, Treatment of Demutualization for Pennsylvania Personal Income Tax (PA PIT) Purposes for additional information regarding the reporting of the transaction and basis determination at time of receipt of the stock. That is if you can prove that the main reason for the home sale falls among health, work, or unforeseeable events. Each digit in the code is part of a series of progressively narrower categories, and the more digits in the code signify greater classification detail. Refer to the What you can do is lower your capital gains taxes further by reducing the amount of your taxable gain.

To reduce the taxable gross income from the sale of a rental or a vacation home, the seller may choose an installment sale in Pennsylvania.. fV(,oQCyPw\ZN jiIPqwr^LaU:\O]

EJNM'cKrFua A loss can occur for property obtained and held for gain, profit or income but is unallowable for personal use property (tangible or intangible). If the property is jointly owned and only one spouse fulfills the qualifications and a joint return is filed, the entire transaction is exempt. Even though the majority of Pennsylvania homeowners are eligible for a capital gains tax break under the tax code, there are still instances when a house is fully taxable. Refer to the information below on the You, your co-owner, spouse, or any resident of the house, The seller or the one who will transfer the property is a. However, the fact that the residence was rented for a couple of months does not necessarily disqualify the residence from the exclusion. The mere assignment of annuity payments to another payee is not taxable as Schedule D gain. Therefore, all transactions displaying net gains and losses are reported on PA Schedule D. If a taxpayer has a loss on personal use property or other property where a loss is not permitted, the transaction must still be reported. Pennsylvania personal income tax does not have a provision for related party transactions. Refer to Personal Income Tax Bulletin 2009-01, Treatment of Demutualization for Pennsylvania Personal Income Tax (PA PIT) Purposes for additional information regarding the reporting of the transaction and basis determination at time of receipt of the stock. That is if you can prove that the main reason for the home sale falls among health, work, or unforeseeable events. Each digit in the code is part of a series of progressively narrower categories, and the more digits in the code signify greater classification detail. Refer to the What you can do is lower your capital gains taxes further by reducing the amount of your taxable gain.  See what we can offer and get cash for your house! Only the actual compensation for the value of the property itself is taxable for Pennsylvania purposes. Refer to the section on. If the funds are not reinvested in the same line of business, then the gains (losses) are reported on PA-40 Schedule D. NAICS is a two- through six-digit hierarchical classification system, offering five levels of detail. However, when a dealer in real property sells real property, the gain is classified under the net profit rules. Catherine aims to educate home sellers, so they can make the best decision for their real estate problems.Shes been featured on a plethora of publications including Better Homes & Gardens, Acorns, Realtor.com, Apartment Therapy, MSN, Yahoo Finance, HomeLight, and Business.com. Pennsylvania personal income tax does PA-19, Sale of Principal Residence worksheet and instructions should be used in order to properly apportion the percentage of a mixed-use property not eligible for the exclusion. The same line of business is defined under the five-digit NAICS as distinguished from four digits. Here are some deductions that may qualify: In order for these deductions to be considered, you should keep receipts, invoices, credit card statements, bills, and other documents that can prove your claims. Proceeds from the sale of intangible assets. Net Gains (Losses) from the Sale, Exchange, or Disposition of Property, Sale of Property Acquired Before June 1, 1971, PA Personal Income Tax Guide - Cancellation of Debt, PA Personal Income Tax Guide - Pass Through Entities, PA Personal Income Tax Guide - Gross Compensation, PA Personal Income Tax Guide -Pass Through Entities, Exchange of Insurance Contracts Under IRC Section 1035, Gain on Distributions of Long-Term Care Policies, Withdrawals from Tuition Account Plans (TAP), Medical Savings Account/Archer (MSA) Distributions, Federal Emergency Management Agency (FEMA), Capital Gain Distributions from Mutual Funds or Regulated Investment Companies, Gain or Loss on the Sale of a Partnership or S Corporation Ownership Interest, IRC 338(h)(10) Sale of Stock Treated as a Sale of Assets, IRC 1256 Mark-to-Market Gains and Losses, IRC 987 and 988 Foreign Exchange Gains and Losses, Other Income from Investment Partnerships, Sales of Land or Buildings Held for Investment, Sales and/or Abandonment of Oil and Gas Wells, Sales of Property Converted from Business or Rental Property to Personal Use Property, Distributions of Stock from Employee Stock Ownership Plans (ESOPs) and Subsequent Sales, Application of Pennsylvania Basis Adjustment Rules for Depreciation, Definition of Sale or Exchange or Other Disposition Under Pennsylvania Law, PA Personal Income Tax Treatment of Stock and Securities Received in a Reorganization, Calculation of Gain or Loss for Taxable Reorganizations, Classification Between Net Profits and Schedule D Gaines (Losses). However, if the promise to pay the future installments is secured by a note that is assignable, the taxpayer may not use the cost recovery method and must report the entire gain during the year of the sale. Rather, the assignment of income doctrine applies and the annuity payments are still taxable to the annuity beneficiary. s&w+i3eNHvoeDfM4n0,4$Azu NZ5kVV[eWJNF"!jZMS:es"o$aT~[GSm5mv?*4Ij$"BUYN[jO,=t;;JCpc! Keystone State. Your home is considered a short-term investment if you own it for less than a year before you sell it. Please tell us how we can make this answer more useful. Gain from the sale of property that has been converted from business or rental property (i.e., income producing property) to personal use property (i.e., non-income producing property) is reported on PA Schedule D. Because the property is personal use when sold, any loss from the sale cannot be claimed for PA personal income tax purposes. If the funds are not reinvested then the gains are reported on PA-40 Schedule D. If the gains are reported as ordinary income on federal Form 4797, it is not necessarily reported as net profits for Pennsylvania personal income tax purposes. Add to this figure the amount of interest payments received during the second year of $1,873 ($7,124 - $5,251). This primarily differs depending on income and one's filing status, whether single, head of household, married filing jointly, or married filing separately. When the sale of stock occurs, the basis is the fair market value of the stock reported as gain in the year of receipt. Lets say you have a $250,000 tax basis in a home youve owned for 5 years that sells for $350,000. However, in such situations, the transaction will show the sales price and basis as the same amount for Pennsylvania personal income tax purposes. For sales of real or tangible personal property, a cash basis taxpayer has the option to either report the entire gain in the year of the sale or report the gain using the installment sales method of accounting. Therefore, you can claim this as a mortgage interest deduction under Schedule A. For Pennsylvania personal income tax purposes, the basis of a life insurance contract must be adjusted to remove the cost of insurance (that is, any costs related to insurance protection). Home sellers usually pay capital gains tax when their property value is appreciated significantly. Refer to You make $100,000 per year and file as single. This exclusion also applies to installment sales. Any gain or loss on the sale, exchange or disposition of stocks or bonds is reportable for Pennsylvania personal income tax purposes. For tax years beginning after Dec. 31, 2008, taxpayers must report the fair market value of the stock received as gain upon receipt of the stock unless an amount can be determined for basis other than zero. endstream

endobj

615 0 obj

<>stream

Basis does not have to be reduced for state purposes merely because the taxpayer utilized a federal tax credit in conjunction with the depreciable asset.

See what we can offer and get cash for your house! Only the actual compensation for the value of the property itself is taxable for Pennsylvania purposes. Refer to the section on. If the funds are not reinvested in the same line of business, then the gains (losses) are reported on PA-40 Schedule D. NAICS is a two- through six-digit hierarchical classification system, offering five levels of detail. However, when a dealer in real property sells real property, the gain is classified under the net profit rules. Catherine aims to educate home sellers, so they can make the best decision for their real estate problems.Shes been featured on a plethora of publications including Better Homes & Gardens, Acorns, Realtor.com, Apartment Therapy, MSN, Yahoo Finance, HomeLight, and Business.com. Pennsylvania personal income tax does PA-19, Sale of Principal Residence worksheet and instructions should be used in order to properly apportion the percentage of a mixed-use property not eligible for the exclusion. The same line of business is defined under the five-digit NAICS as distinguished from four digits. Here are some deductions that may qualify: In order for these deductions to be considered, you should keep receipts, invoices, credit card statements, bills, and other documents that can prove your claims. Proceeds from the sale of intangible assets. Net Gains (Losses) from the Sale, Exchange, or Disposition of Property, Sale of Property Acquired Before June 1, 1971, PA Personal Income Tax Guide - Cancellation of Debt, PA Personal Income Tax Guide - Pass Through Entities, PA Personal Income Tax Guide - Gross Compensation, PA Personal Income Tax Guide -Pass Through Entities, Exchange of Insurance Contracts Under IRC Section 1035, Gain on Distributions of Long-Term Care Policies, Withdrawals from Tuition Account Plans (TAP), Medical Savings Account/Archer (MSA) Distributions, Federal Emergency Management Agency (FEMA), Capital Gain Distributions from Mutual Funds or Regulated Investment Companies, Gain or Loss on the Sale of a Partnership or S Corporation Ownership Interest, IRC 338(h)(10) Sale of Stock Treated as a Sale of Assets, IRC 1256 Mark-to-Market Gains and Losses, IRC 987 and 988 Foreign Exchange Gains and Losses, Other Income from Investment Partnerships, Sales of Land or Buildings Held for Investment, Sales and/or Abandonment of Oil and Gas Wells, Sales of Property Converted from Business or Rental Property to Personal Use Property, Distributions of Stock from Employee Stock Ownership Plans (ESOPs) and Subsequent Sales, Application of Pennsylvania Basis Adjustment Rules for Depreciation, Definition of Sale or Exchange or Other Disposition Under Pennsylvania Law, PA Personal Income Tax Treatment of Stock and Securities Received in a Reorganization, Calculation of Gain or Loss for Taxable Reorganizations, Classification Between Net Profits and Schedule D Gaines (Losses). However, if the promise to pay the future installments is secured by a note that is assignable, the taxpayer may not use the cost recovery method and must report the entire gain during the year of the sale. Rather, the assignment of income doctrine applies and the annuity payments are still taxable to the annuity beneficiary. s&w+i3eNHvoeDfM4n0,4$Azu NZ5kVV[eWJNF"!jZMS:es"o$aT~[GSm5mv?*4Ij$"BUYN[jO,=t;;JCpc! Keystone State. Your home is considered a short-term investment if you own it for less than a year before you sell it. Please tell us how we can make this answer more useful. Gain from the sale of property that has been converted from business or rental property (i.e., income producing property) to personal use property (i.e., non-income producing property) is reported on PA Schedule D. Because the property is personal use when sold, any loss from the sale cannot be claimed for PA personal income tax purposes. If the funds are not reinvested then the gains are reported on PA-40 Schedule D. If the gains are reported as ordinary income on federal Form 4797, it is not necessarily reported as net profits for Pennsylvania personal income tax purposes. Add to this figure the amount of interest payments received during the second year of $1,873 ($7,124 - $5,251). This primarily differs depending on income and one's filing status, whether single, head of household, married filing jointly, or married filing separately. When the sale of stock occurs, the basis is the fair market value of the stock reported as gain in the year of receipt. Lets say you have a $250,000 tax basis in a home youve owned for 5 years that sells for $350,000. However, in such situations, the transaction will show the sales price and basis as the same amount for Pennsylvania personal income tax purposes. For sales of real or tangible personal property, a cash basis taxpayer has the option to either report the entire gain in the year of the sale or report the gain using the installment sales method of accounting. Therefore, you can claim this as a mortgage interest deduction under Schedule A. For Pennsylvania personal income tax purposes, the basis of a life insurance contract must be adjusted to remove the cost of insurance (that is, any costs related to insurance protection). Home sellers usually pay capital gains tax when their property value is appreciated significantly. Refer to You make $100,000 per year and file as single. This exclusion also applies to installment sales. Any gain or loss on the sale, exchange or disposition of stocks or bonds is reportable for Pennsylvania personal income tax purposes. For tax years beginning after Dec. 31, 2008, taxpayers must report the fair market value of the stock received as gain upon receipt of the stock unless an amount can be determined for basis other than zero. endstream

endobj

615 0 obj

<>stream

Basis does not have to be reduced for state purposes merely because the taxpayer utilized a federal tax credit in conjunction with the depreciable asset.  Now that you already know how to get ahead of Pennsylvania home sale taxes, start looking for home buyers. Tax Rates Pennsylvania Department of Revenue > Tax Rates Current Tax Rates For detailed and historic tax information, please see the Tax Compendium. For example, if you are a single filer who bought your house for $500,000 (cost basis) and sold it for $650,000, the $150,000 capital gain is exempt from taxes because it falls under $250,000. The A repossession of property occurs when there is a transfer of property under a deferred payment contract and there is a default under the contract. After figuring out your tax basis, you would subtract this from the profits to determine the amount you owe taxes on. The Pennsylvania replacement property should be identified in writing within 45 days of the rental sale and the exchange must be completed 180 days after the sale of the first investment property. Rather, the cash basis taxpayer may report the entire gain in the year of the sale or use the cost recovery method of accounting (each installment payment is attributable to basis until fully recovered) to determine the gain on each installment payment. The policyholder is entitled to receive consideration for giving up membership interests under their policy with the mutual insurance company. Gain from bartering is the difference between the adjusted basis of the relinquished property and the fair market value of the property received. For Pennsylvania personal income tax purposes prior to Jan. 1, 2005, the entire cash surrender value of an insurance policy or annuity less premiums paid (other than the premiums on the coverage on the persons life under the insurance contract) was taxed in the income class net gains or income from disposition of property, rather than as interest. ET Estimated tax penalties can be up to 20% of your gain as of 2021. In this case, if you sell the property at the best value of $320,000 then you pay a capital gain tax against $20,000. For example, a taxpayer lived in their primary residence for ten years. Examples include a sole proprietors residence above the sole proprietors store, an office in home and a duplex where one unit is rented. 720 0 obj

<>/Filter/FlateDecode/ID[]/Index[611 455]/Info 610 0 R/Length 217/Prev 636005/Root 612 0 R/Size 1066/Type/XRef/W[1 3 1]>>stream

PA Schedule 19 must be included with the return. Generally, gain (loss) on sales or other dispositions of property is computed by subtracting the adjusted basis of a property from the value of cash and property realized on its sale or disposition. In computing income, a depreciation deduction shall be allowed for the exhaustion, wear and tear and obsolescence of property being employed in the operation of a business or held for the production of income.

Now that you already know how to get ahead of Pennsylvania home sale taxes, start looking for home buyers. Tax Rates Pennsylvania Department of Revenue > Tax Rates Current Tax Rates For detailed and historic tax information, please see the Tax Compendium. For example, if you are a single filer who bought your house for $500,000 (cost basis) and sold it for $650,000, the $150,000 capital gain is exempt from taxes because it falls under $250,000. The A repossession of property occurs when there is a transfer of property under a deferred payment contract and there is a default under the contract. After figuring out your tax basis, you would subtract this from the profits to determine the amount you owe taxes on. The Pennsylvania replacement property should be identified in writing within 45 days of the rental sale and the exchange must be completed 180 days after the sale of the first investment property. Rather, the cash basis taxpayer may report the entire gain in the year of the sale or use the cost recovery method of accounting (each installment payment is attributable to basis until fully recovered) to determine the gain on each installment payment. The policyholder is entitled to receive consideration for giving up membership interests under their policy with the mutual insurance company. Gain from bartering is the difference between the adjusted basis of the relinquished property and the fair market value of the property received. For Pennsylvania personal income tax purposes prior to Jan. 1, 2005, the entire cash surrender value of an insurance policy or annuity less premiums paid (other than the premiums on the coverage on the persons life under the insurance contract) was taxed in the income class net gains or income from disposition of property, rather than as interest. ET Estimated tax penalties can be up to 20% of your gain as of 2021. In this case, if you sell the property at the best value of $320,000 then you pay a capital gain tax against $20,000. For example, a taxpayer lived in their primary residence for ten years. Examples include a sole proprietors residence above the sole proprietors store, an office in home and a duplex where one unit is rented. 720 0 obj

<>/Filter/FlateDecode/ID[]/Index[611 455]/Info 610 0 R/Length 217/Prev 636005/Root 612 0 R/Size 1066/Type/XRef/W[1 3 1]>>stream

PA Schedule 19 must be included with the return. Generally, gain (loss) on sales or other dispositions of property is computed by subtracting the adjusted basis of a property from the value of cash and property realized on its sale or disposition. In computing income, a depreciation deduction shall be allowed for the exhaustion, wear and tear and obsolescence of property being employed in the operation of a business or held for the production of income.  Refer to the If the seller/creditor experiences a gain to the extent that the FMV is greater than the basis or a loss to the extent the FMV is less than the basis. Losses are not recognized on the sale of property that was not acquired as an investment or for profit such as The first two digits designate the economic sector; The third digit designates the subsector; The fourth digit designates the industry group; The fifth digit designates the NAICS industry; and. And you are not liable for any capital gain taxes on an inherited property. Refer to Pennsylvania Tax Reform Code Section 303(a)(3)(iv) for additional information. When the acquiring party disposes of the property, the original cost basis will be used. Demutualization is the conversion of a mutual insurance company to a stock insurance company. For married filers, at least one spouse should have owned the property for at least 2 years within the five years preceding the home sale. WebSALE OF YOUR PRINCIPAL RESIDENCE AND PA PERSONAL INCOME TAX IMPLICATIONS Generally, homeowners who owned and used their homes as principal 61 Pa. Code 125.41-125.43 for further information. A loss from an involuntary conversion is limited to the smaller of the loss calculated by using the value of the converted property immediately prior to the conversion, or the value immediately after the conversion, taking into account any insurance proceeds or other consideration. For tax years 2018 and 2019, gains invested in Qualified Opportunity Funds are required to be reported for PA personal income tax purposes even though the gains are deferred for federal income tax purposes. However, if the monies were not fully reinvested into the damaged property, the excess would be taxable on PA-40 Schedule D. To the extent FEMA money was not used to restore the property, it would be offset by a basis reduction. [1] Let's say, for example, that you A simple capital gains calculation looks like this: adjusted gross proceeds from the sale of a qualified capital asset (say $200,000) minus the adjusted original purchase price of that property (say $150,000) equals a $50,000 capital gains amount. No. Here, we'll take a look at all the nitty-gritty of capital gains taxes including their rate, how you can avoid it, partial exclusion, and more! If only part of the payment obligation under the contract is discharged by the repossession, figure the basis using only that amount instead of the full face value of the contract.). This only applies to dealers in real property. Refer to Of course, there are certain requirements for you to be eligible for this exemption: Note that you don't have to live on the Pennsylvania property for two consecutive years. Generally, homeowners who owned and used their home as their principal residence for at least two of the five years prior to the date of sale will qualify for the exclusion on a sale of their home. There are no provisions for long-term and short-term gains. Long-term capital gains tax rates are almost always lower than short-term capital gains. In applying this classification rule, consideration is given whether that new real property is geographically located near the dealers old property.